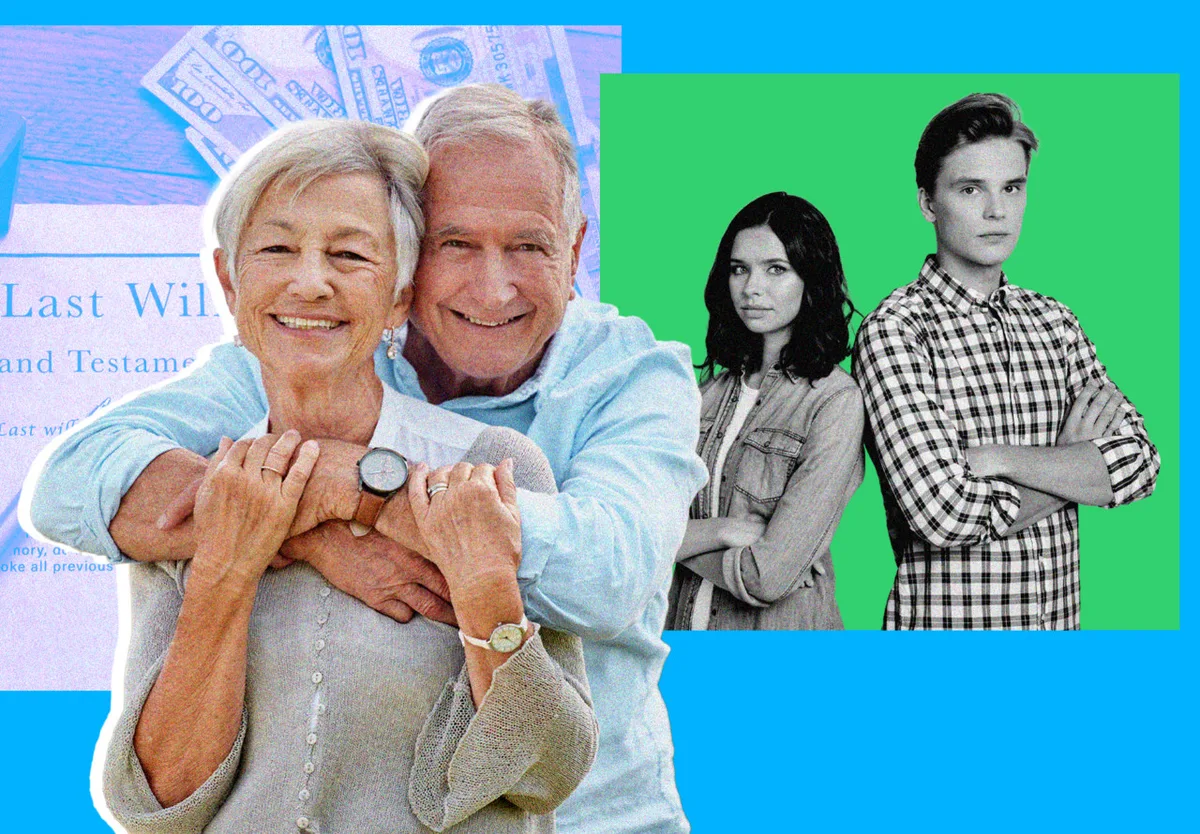

How to Protect Your Inheritance When a Parent Remarries

A parent's new romance can reshape your inheritance overnight. Here's how to have the money talk before it's too late.

Your aging parent just found love again — great for them, potentially costly for you. Before wedding bells ring, there's a real financial conversation that needs to happen, and waiting too long could mean your inheritance evaporates into a blended-family situation you never saw coming.

Estate planning is the core issue here. When a widowed or divorced parent remarries without updating their will, trust, or beneficiary designations, their new spouse can legally end up with assets you expected to inherit. It's not cynical to think about this — it's just smart money management, the same way you'd rebalance a portfolio before a market shift.

Read more Mortgage Demand Slumps as Rates Stay Stuck in Tight Range →

The trick is framing. Nobody wants to look like they're already counting their parent's money. Approach the conversation as concern for *their* wishes being carried out correctly — because that's actually true. Ask whether they've reviewed their estate documents recently. Ask if they've talked to an estate attorney. Let them lead. You're just opening the door.

Key documents to flag: wills, revocable living trusts, retirement account beneficiary forms, and life insurance policies. These don't automatically update when someone gets remarried, and in many states the law will override an outdated will in ways that favor the new spouse. A few hours with an estate attorney now can lock in your parent's actual intentions before emotions and new relationships complicate everything.

Bottom line — this is one of those situations where doing nothing is itself a high-risk move. The earlier you have the conversation, the less awkward it is, and the more options your parent has to structure things fairly for everyone involved. Continue reading at MarketWatch.com